Understanding investment risks

Understanding investment risks

Section Heading

All investing involves risk

In seeking higher returns for your super, the trade-off is taking on increased risk.

Generally, shares and property have higher risk and higher expected returns than fixed interest and cash. Therefore, the asset mix in each investment option is important in assessing the option’s expected return and risk.

“Risk” means the change in value of investments away from expectations. The value of higher risk investments fluctuates more widely and frequently and is more likely to result in loss of value than lower risk investments. Each investment option has a different risk profile.

The value of investments is influenced by many factors, such as economic and market conditions, government policy, interest rates, currency movements, inflation and the performance of the fund managers engaged by Funds SA.

The expectation of negative returns

One of the most important concepts to consider when making an investment decision is that of risk and return. All investments, including super, have some level of risk.

Members should be aware capital losses are possible, depending on the investment option(s) chosen and their performance over time. Fluctuations in investment markets will have on-going impacts on performance. This volatility is a normal part of investing and can occur with money you may have in other super funds, the share market, and other types of investment.

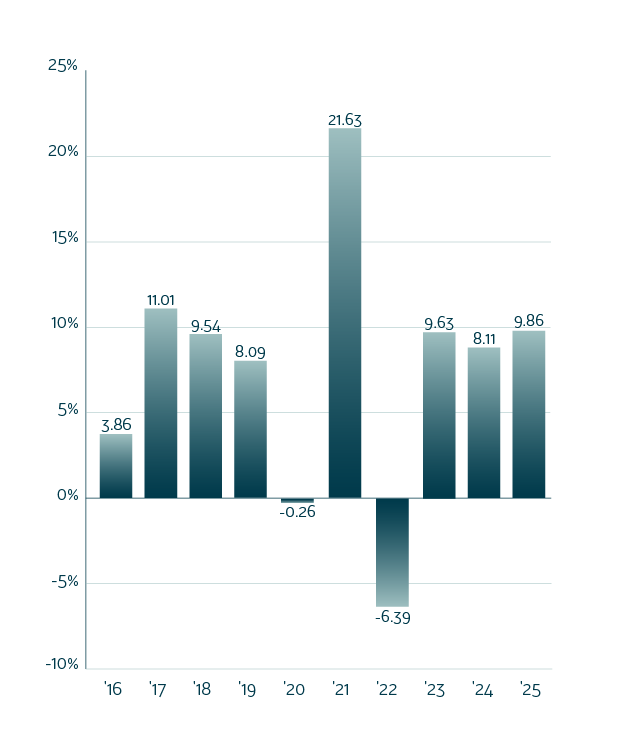

Each option’s investment objective provides an indication of risk by stating the number of negative annual returns likely to be experienced over any 20-year period. For example, for the Triple S Balanced Investment option, it is expected the investment strategy will result in between four to six negative annual returns over any 20-year period. This means the risk of a negative return in any single year is between 20% and 30%. Chart 1 below illustrates the annual returns of the Triple S Balanced Investment option over the last 10 years.

Looking back over the history of the Triple S Balanced Investment Option, it has recorded a negative return for financial year periods four times. This is in line with expectations (4 to 6 years in 20).

The expected range of annual return outcomes also provides an indication of risk. This varies between the options. Generally, options with the highest potential long-term returns also come with the widest range of returns including the possibility of negative returns. Options with the lowest potential long-term returns come with the narrowest range of returns and the greatest likelihood of positive returns. Each of Super SA’s investment options has a different level of risk and return, as shown in Chart 2 below.

Chart 1: Triple S Balanced option annual returns to 30 June 2025*

Returns net of fees and gross of tax

Chart 2: Expected range of returns over a 1-year period*

*Note there is approximately a 5% chance the return could lie outside of this range.

Understanding your attitude to risk is important and this may change over time. You may wish to periodically review your investment strategy to make sure it still meets your needs.Switching your investment option is an important decision

It’s not easy to time entry to, or exits from, markets. Selling out of more risky options (i.e. those options with larger allocations to assets such as shares and property) and switching into less risky options (such as cash and options with higher allocations to fixed interest) can be costly over the longer term as it effectively locks in the losses which result from poor investment markets. As well, it is possible to miss out on future growth by being out of the market when it recovers. We understand you may be concerned about the impact of market movement on your super. We encourage you to think about your super as a long-term investment generating a return over multiple years. We suggest you don’t focus narrowly on short-term results. Many members seek professional financial advice, especially those members approaching or in retirement. There are a number of investment options offered by Super SA to suit members with differing risk appetites and time horizons.Types of investment risks to consider

Inflation risk

Inflation may exceed the return you receive on your investment.

Market risks

Economic, technological, political or legal conditions may affect the value of investments. Market sentiment may also alter the value.

Manager performance risks

The risk that individual investment managers under-perform.

Change in interest rates may also affect investment returns positively or negatively.

Foreign currency risk

For overseas investment there is a risk that the value of other currencies may change in relation to the Australian dollar and reduce the value of the investment.

Derivatives are financial contracts used in the management of investments whose value depends on the value of specific underlying investments. Their value can fluctuate, sometimes away from the expected value, and they are also subject to counterparty risk.

Counterparty risk

Counterparty risk is the risk that an organisation contracted to provide an investment service is not able to do so. This may result in loss of value.

Underlying investment risk

The value of each option’s underlying investments can rise and fall. Some of the most common influences on underlying investments include:- Australian shares: Individual shares are affected by factors affecting the share market generally and also by the profits and expected profits of individual companies.

- International shares: There are similar risks as for Australian shares. Additionally, they are affected by political factors and the currency exchange rate of the country where the shares are held.

- Property: Economic factors such as inflation and unemployment will affect the return on property as well as the location and quality of the property itself.

- Diversified fixed interest investments: Changes in interest rates, as well as the risk of loan repayment default, will result in a change in value of this investment.

Other risks specific to super investments include changes to super or taxation laws, which may affect the accessibility or value of your investment.

Performance and risk are closely linked when talking about investments. Generally, the investment options that offer the highest long term performance may also carry the highest level of short term risk, and vice versa.

Choosing the right options

Your investment choice is unique to you.When you join Triple S, your super is automatically invested in the Balanced option. In fact, over 90% of Triple S members are in this option. However, your super is unique to you and this means the Balanced option may not always be suited to you.

Before choosing an investment option, think about:

• Your current financial position

• Your age

• When you plan to retire

• How long your super will need to last you in retirement

• Your risk and return preferences.

Each option has different objectives, risk and characteristics for you to consider. You can take our Risk profiler quiz to get to know your risk profile, and better understand which investment option is right for you. Your profile will come with an explanation, and you can keep it for future reference.

Your super, your choice

For financial planning advice, speak to a licenced financial planner. You can visit the Financial Advice Association Australia (FAAA) website https://faaa.au/ and access their “Find a Planner” service to locate an FAAA member near you.